The idea of a comfortable retirement means different things to different people. Whether that is bi-annual overseas holidays (when Covid permits), improving your golf skills or just pottering in the garden everyone has their own version of comfortable.

The latest ABS data highlights that life expectancy in Australia continues to increase, with an Australian male aged 50 years can expect to live another 32.9 years, and a female another 36.3 years. When we overlay this with the average retirement age of 55.4 years there is the potential for a widening age gap and with it a retirement funding gap.

The Association of Superannuation Funds of Australia (ASFA) has recently released its own set of figures highlighting what the amount of superannuation they believe people need to accumulate through various age brackets in their life and how much people will require (in today’s dollars) to live a comfortable retirement.

ASFA Retirement Standard: https://www.superannuation.asn.au/resources/retirement-standard

ASFA Retirement Standard: https://www.superannuation.asn.au/resources/retirement-standard

Having the perspective of where the age pension sits relative to the minimum wage and a ‘comfortable retirement’ should provide guidance and motivation for the working population in seeking where potential shortfalls exist in their own circumstances and understanding the mechanisms to bridge any gap. If you envision a retirement lifestyle above that provided by the Age Pension and the benefits of Super Guarantee, then a proactive approach towards your retirement planning is a vital consideration.

1. “Experience to date with the early release of superannuation.” The Association of Superannuation Funds of Australia (ASFA). June 2020.

2. “Super Balance Detective.” The Association of Superannuation Funds of Australia (ASFA). Accessed January 2021.

1. “Experience to date with the early release of superannuation.” The Association of Superannuation Funds of Australia (ASFA). June 2020.

2. “Super Balance Detective.” The Association of Superannuation Funds of Australia (ASFA). Accessed January 2021.

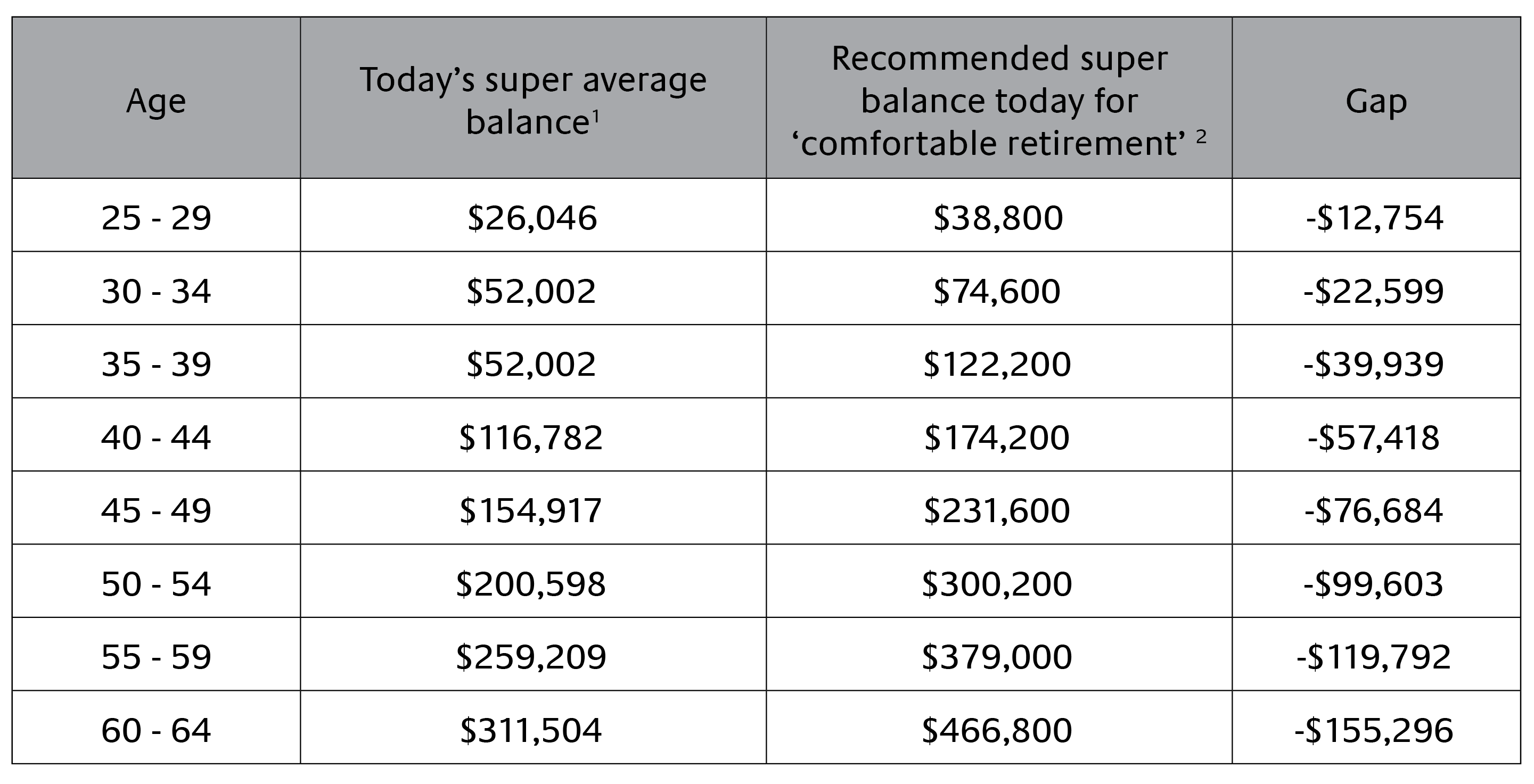

The table above suggests (that on average) there’s a potential shortfall in today’s super balances to be on track for a ‘comfortable retirement’ and shows where your super balance should be at your age today. Example: For those in the 40–44 age group, the balance shortfall is estimated at over $57,000. And for those in their early sixties, the balance shortfall is estimated at over $155,000.

What can I do if there’s a gap?

Importantly, you aren’t alone. We can help point you in the right direction with an appropriately designed road map aligned with your personal circumstances, and provide you with a helping hand along the way.

To review this further, please contact Phillip Bures on 1300 795 515 or your principal adviser.

This article contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information. If you decide to purchase or vary a financial product, your financial adviser, Hillross Financial Services Limited and other companies within the AMP Group may receive fees and other benefits. The fees will be a dollar amount and/or a percentage of either the premium you pay or the value of your investments. Please contact us if you want more information. Prosperity Wealth Advisers Pty Ltd (ABN 32 141 396 376), is an Authorised Representative and Credit Representative of Hillross Financial Services Ltd, Australian Financial Services Licensee and Australian Credit Licensee.

*Includes pension and energy supplement, as at March 2021.

The table below shows the average super balances of Australians across different age groups and genders. These recommended super balances have been provided by ASFA, averaged across different age groups and are designed to guide individuals on the amount of accumulated superannuation an individual requires to be on track for a ‘Comfortable retirement'

With superannuation balances being closely linked to paid work it’s also worth noting that Australian females on average have less in their super than males with the tendency for women to have prolonged periods out of the workforce to raise families impacting accumulated balances.

A good way to see how your own super balance stacks up both against the current average balance for your age group as well as ASFA’s suggested average balance is to log into your super account and review your balance. If you identify a gap between your own accumulated balance and your peer group it is important to recognise this and take the necessary action.

(i) Age Pension (Publicly Funded) whereby the Government pays an income support payment, the Age Pension, to senior Australians who meet eligibility tests with regards to age, residency, income and assets. The Age Pension is paid fortnightly be the Department of Social Security (DSS) through its agency Centrelink. Eligibility Age is gradually increasing to 67 from 1 July 2023 onwards (DOB 01/01/1957 onwards).

(ii) Super Guarantee (compulsory private savings) - this is compulsory private saving; a reasonable minimum share of an employee’s income that is saved to contribute additional resources to their retirement.

(iii) Voluntary Savings (voluntary private savings) which are over and above the mandatory Super Guarantee contributions, there are numerous tax incentives for individuals to make additional voluntary contributions to the super environment. These incentives are seen not only in the contribution options available in accumulation phase, but also the tax treatment of super benefits in both accumulation and retirement phase.

Australia’s retirement income system, which takes a three-pillar approach, has been pursued by the Government to guide peoples funding of their retirement income requirements being:

(i) Age Pension (Publicly Funded) whereby the Government pays an income support payment, the Age Pension, to senior Australians who meet eligibility tests with regards to age, residency, income and assets. The Age Pension is paid fortnightly be the Department of Social Security (DSS) through its agency Centrelink. Eligibility Age is gradually increasing to 67 from 1 July 2023 onwards (DOB 01/01/1957 onwards).

Being informed on how the Government intersects with the individual is important. Recognising your budget, balance and future potential income needs and expenses (renovations, gifts to grandchildren and aged care) as early as possible can ensure you are well prepared for a successful retirement.

1) Take advantage of the tax concessions to contribute funds to superannuation – there are numerous opportunities available to individuals to contribute funds to superannuation in a tax effective way. As always it is important to understand which opportunities are specifically relevant to your circumstances.

2) Review and consolidate your superannuation accounts - Millions of Australians have more than one super account. If you’re one of these people, it’s worth thinking about consolidating them into one account. The money you may save in multiple fees could stay invested and really help grow your overall super balance.

3) Understand and review your investment strategy – Understanding the relationship between risk and return in the formative years of your working life can leave you in good stead leading into retirement. The inability to access your superannuation balance until later years in your life may leave you feeling like you are ‘missing out’ however within investment parlance this presents a time arbitrage allowing your retirement balance to be able to withstand the volatility of financial markets