Focusing on leases, the new Australian Accounting Standard AASB 16 came into effect for financial periods beginning on or after 1 January 2019.

For entities with 30 June balance dates, the first financial report affected will be 30 June 2020. However, ASIC and other regulators are pushing for 30 June 2019 reports to disclose the likely impact of the new standard.

Importantly, AASB 16’s regulatory impact is wider than listed companies. It also covers entities preparing general purpose financial statements or applying the recognition and measurement principles of the Australian accounting standards. This means that listed companies, large private companies, companies limited by guarantee, and government entities are all impacted.

So what changes?

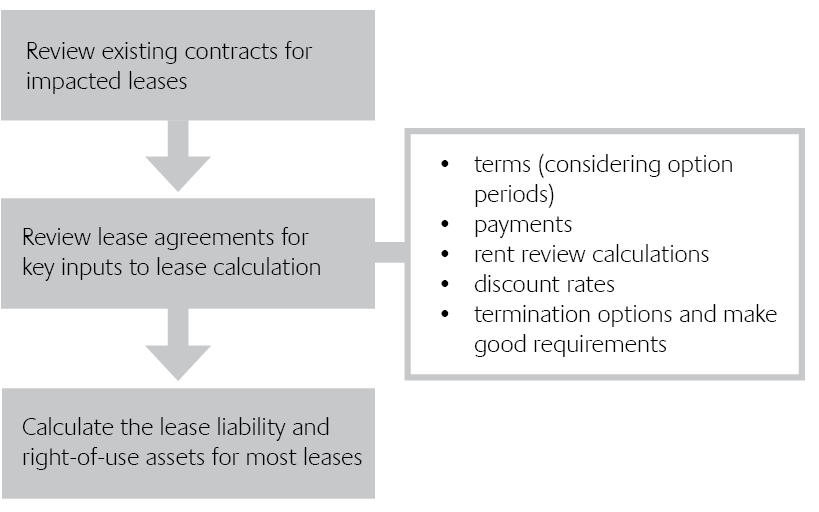

The Standard’s new model requires lessees to recognise all leases on balance sheet, except for short-term leases and leases of low value assets.

To illustrate, consider a business’ leased premises. AASB 16 requires the lease liability to be recognised on the balance sheet additional to a “right-to-use” asset, rather than the previous method of expensing the rental payments monthly. Further, the asset will be depreciated/amortised and the lease liability reduced each month aligned to payments. This will significantly alter the structure of balance sheets and profit or loss statements.

This fundamental change has led many to suggest that as much as $100 billion of lease liabilities (and their corresponding asset) will be brought on balance sheet for ASX listed companies.

And more

Significantly, this new standard will increase board and management scrutiny of leases in using to obtain assets and determining which should be bought rather than leased.

Additional considerations could also include remuneration schemes, data systems, gearing and loan covenants, and stakeholder engagement.

What needs to be done?

Given the looming deadline, now is the time for management to ask numerous questions to safeguard AASB16 compliance.

Prosperity can help with our “readiness assessment”

Our review provides assurance that preparation for AASB 16’s implementation will minimise risks associated with accuracy and timeliness of financial reporting and stakeholder communication (shareholders, lenders, regulators etc).

If you would like more information, please contact Alex Hardy on 0419 997 403 or your principal adviser.